Exhibit 10.15

| This is the 1st affidavit of Tim Conder in this case and was made on November 6, 2025 NO. SE258388 VANCOUVER REGISTRY |

IN THE SUPREME COURT OF BRITISH COLUMBIA

IN THE MATTER OF THE COMPANIES’ CREDITORS ARRANGEMENT ACT,

R.S.C. 1985, c. C-36

AND

IN THE MATTER OF THE BUSINESS CORPORATIONS ACT, S.B.C. 2002, c. 57

AND

IN THE MATTER OF A PLAN OF COMPROMISE OR ARRANGEMENT OF

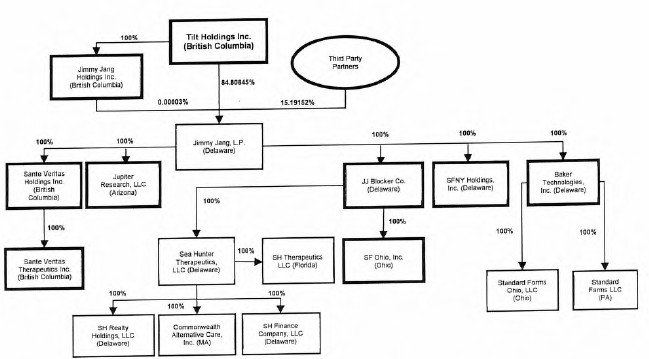

TILT HOLDINGS INC.

PETITIONER

AFFIDAVIT

I, Tim Conder, businessperson, of the City of Reno, Nevada, United States of America, SWEAR THAT:

I. | INTRODUCTION |

1.I am the Chief Executive Officer of TILT Holdings Inc. (the “Petitioner”) and have personal knowledge of the matters described in this affidavit, except where I say that my knowledge is based on information from others, in which case, I believe the same to be true. I am authorized to make this affidavit on behalf of the Petitioner.

2.I have provided the loan documents, guarantees, security documents, and other related documents referenced herein to the Petitioner’s legal counsel, McCarthy Tetrault LLP, and copies of same (other than those documents attached as exhibits to this affidavit) are attached to the first affidavit of Susan Danielisz (the “Danielisz Affidavit”). I have reviewed the Danielisz Affidavit.

3.This affidavit is sworn in support of a petition by the Petitioner dated November 7, 2025 for an initial order (the “Initial Order”) under the Companies’ Creditors Arrangement Act, R.S.C. 1985, c C-36 (the “CCAA”).